Weekly Newsletter Vol.2

Welcome to the second edition of our weekly newsletter where we follow up with the aftermath of Stream Finance's events and the discussions that sparked around accountability in DeFi.

Accountability in DeFi

Over the last week there has been a huge debate brewing on our timeline, to sum it up, we use the phrase ‘accountability in DeFi’

Building on what we discussed last week, the lending market has been under a lot of scrutiny especially the part where curators/allocators are supposed to be more accountable for the risk exposure they give to investor funds.

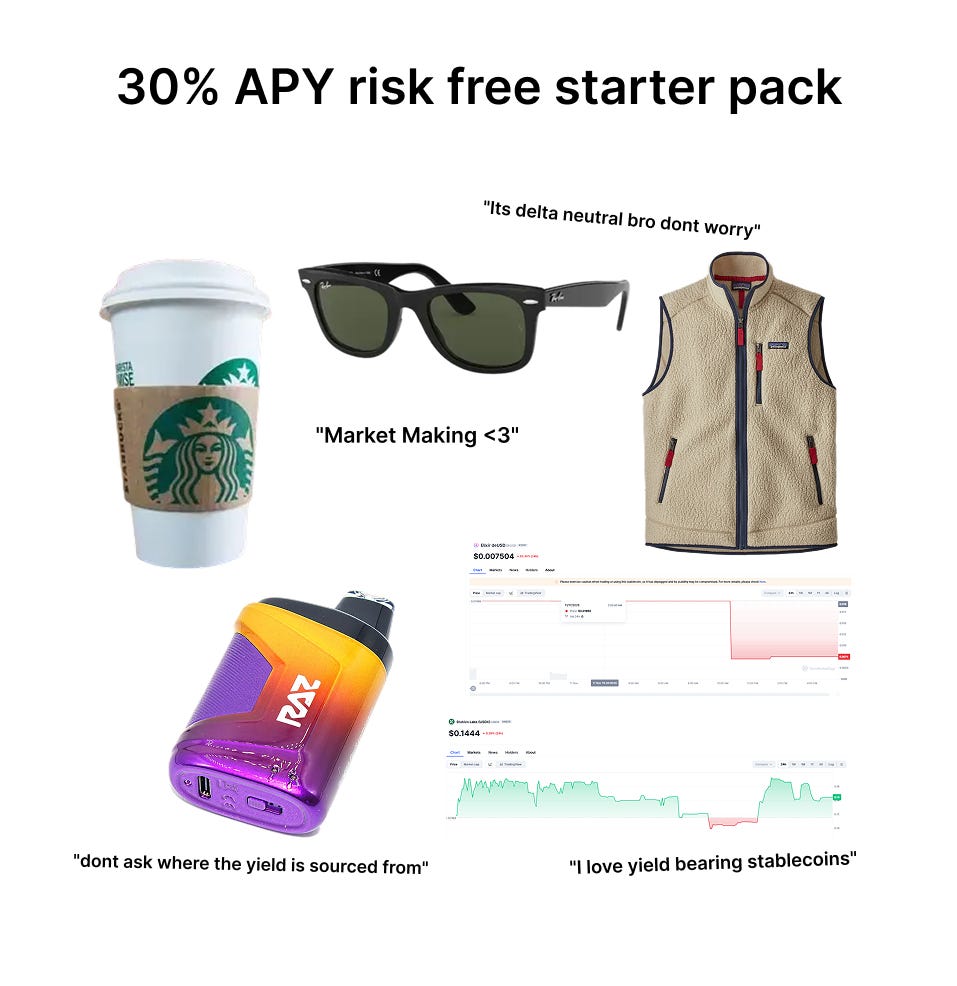

At the beginning of it all, tokenization and abstraction for institutional trading strategies seemed like the way to go for DeFi, which started with packaging delta-neutral hedging strategies (holding crypto long while shorting perpetual futures) into USDe, a synthetic dollar that has grown to become the third-largest stablecoin with over $3.5B in TVL, Ethena’s tokenized basis trades, democratizing investment instruments which were historically only limited to institutions, further leading the whole way for yield-products to come.

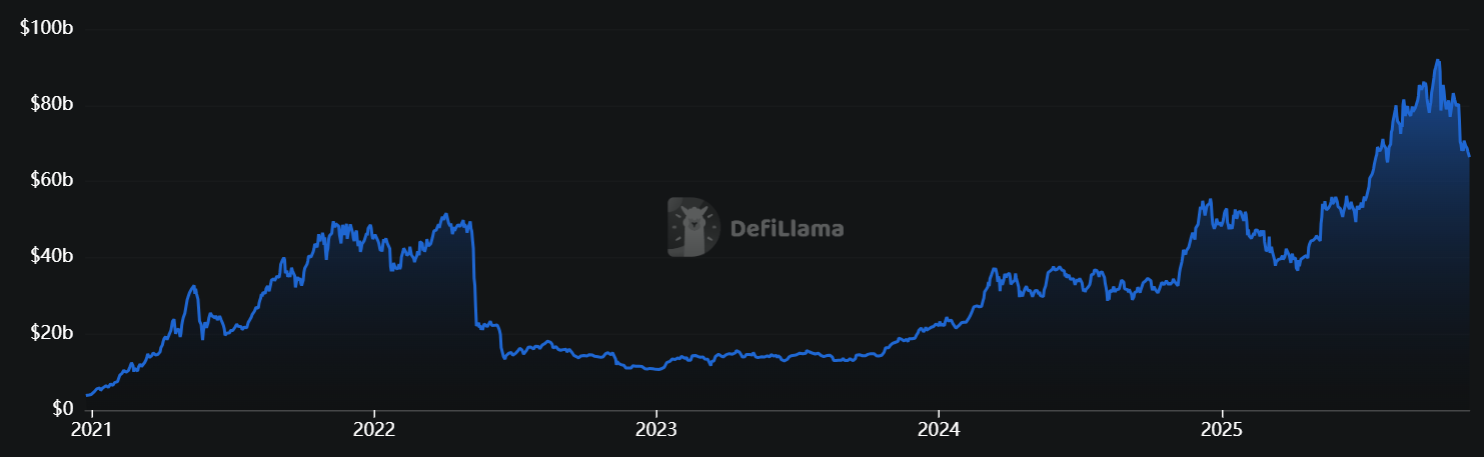

Lending protocols have over $66 billion in TVL.

How much of it is traceable?

How much of it is deployed in shady strategies?

These questions are becoming increasingly relevant due to recent events, let’s break them down one by one, and offer a solution too.

Meet Risk Curators and Onchain Capital Allocators (OCCAs)

Although these are two different terms they achieve the same finality, putting yield-bearing strategies together, OCCAs do it in the form of strategy-branded products and risk curators deploy in modular money markets.

The Stream Finance Crisis: A Turning Point

On November 4th, 2024 (which began surfacing on October 10th with early warning signs), Stream Finance disclosed that an external fund manager had lost approximately $93 million in user funds.

Stream’s stablecoin xUSD immediately depegged, crashing from $1 to as low as $0.18 — an 82% collapse.

The contagion spread quickly: DeFi research group Yields and More identified nearly $285 million in direct debt exposure across lending protocols including Morpho, Euler, Silo, Gearbox, and Elixir Network with curators like Re7 Labs, TelosC and MEV Capital among the most exposed.

This crisis exposed fundamental flaws in how DeFi handles risk curation.

The incident highlighted how the narrative towards yield-bearing instruments is going against the core ethos of DeFi and inclining towards opaque black-box models that were prevalent in TradFi.

This led to a much needed question that Chaos Labs articulated perfectly in their analysis “DeFi’s Black Box: How Risk & Yield Are Repackaged”:

“The rise of OCCAs and risk curators is a predictable outcome of DeFi’s structured products phase. Once Ethena showed that desk-grade strategies could be tokenized and distributed, a layer of professional allocators was bound to form around money markets. This layer is not inherently a problem. The problem arises when the operational discretion it requires becomes a substitute for verifiability.”

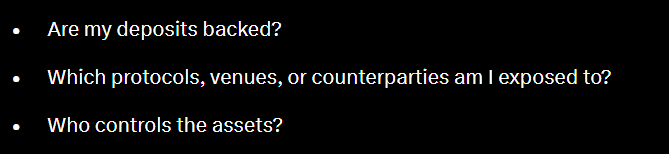

Chaos Labs outlined three critical questions every DeFi investor must be able to answer:

The Stream Finance collapse demonstrated what happens when these questions can’t be answered clearly.

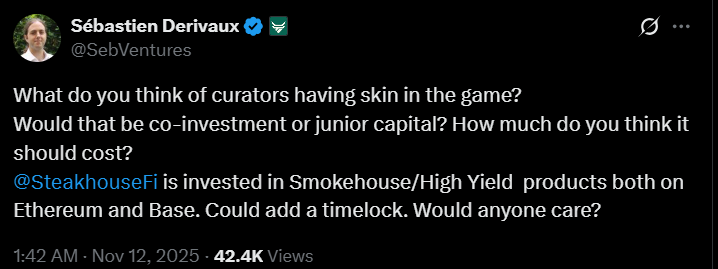

What do we think of curators having skin in the game

There are two approaches to this:

1) Co-investment: Curators invest alongside LPs on equal terms. While this aligns incentives, it doesn’t differentiate between curator expertise and general investor risk. Curators face the same downside as everyone else, but their specialized knowledge doesn’t translate into appropriate risk-reward positioning.

2) Junior Capital: Curators take the first-loss position in a waterfall structure. If defaults occur, curator capital is depleted first before LP funds are touched. This is the superior model because:

Our opinion is that it should be part of the junior capital stack rather than co-investment.

Curators have the best understanding of the underlying risk in a vault, hence they are the most equipped to take junior risk, and the yield will be proportionally higher too.

The size of junior can be set to the underlying default probability, alongside incentivization this can reduce adverse selection greatly.

Along with this, popular countermeasures would be:

1) Transparent Reserves: This is of utmost importance as we saw how only $150M out of the claimed $500M of Stream’s TVL were traceable

2) Better Rehypothecation: The reuse of collateral is inherent to products like insurance or restaking. Rehypothecation should be limited and disclosed to avoid circular mint-and-lend loops across affiliated products.

3) ACTUAL Decentralization: on paper we all think that all DeFi protocols are decentralized, but systemic risk reveals otherwise, any protocol should prioritize risk isolation and better practices to prevent such market events

In the grand scheme of things, one might say that DeFi is taking after TradFi issues all over again, but iteration by iteration we can achieve sophistication while eliminating the black box problem.

Moving along to a more positive note, we saw JPMorgan allow their clients to swap JPMD (JPMorgan’s Deposit Token) for USDC on Base.

JPMorgan has been known in the Web3 space for either Kinexys (fka. Onyx) or Jamie Dimon’s snarky comments towards the industry, with the latter gaining much more traction.

This step is a positive one as JPMorgan moves from using blockchain rails in a closed loop to an open loop ecosystem

Now, why would banks do this?

Banks still get to run their closed systems with their own deposit tokens (under their own custody and compliance) while Coinbase keeps custody of their stablecoins.

A fun fact is, under the GENIUS Act, stablecoins like USDC cannot dish out interest/yield natively to their holders, but with tokenized deposits you can very well expect JPMorgan to incorporate interest-based mechanisms for holders.

How this translated into stablecoin adoption is a story yet to unfold, but this is indeed a step in the right direction for an onchain economy.

Until next time

~ Team Qiro